Understanding the Connection Between Inflation and Interest Rates

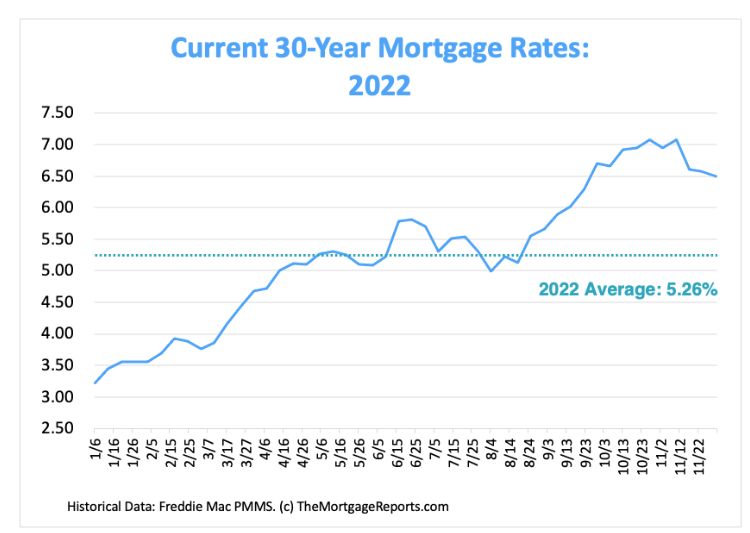

Well, 2022 is over and it’s been another wild and crazy year. 2022 saw inflation start at 7 percent then rise as high as 9.1 percent only to ease back down to 7.1 percent in December.

At the same time mortgage interest rates started the year off at around 3 percent and ended the year at 6.50 percent, more than doubling over that time period. At the same time, the stated inflation was only 0.1 percent higher at years end. There was not a 1-to-1 correlation between the two.

What about home prices? Home prices nationwide were up 2.6% year-over-year in November. But what’s interesting is that they seem to have followed the inflation rate by moving higher mid-year and easing down at year’s end.

While some pundits scream for lower prices or even a crash due to rising interest rates, it appears they may be too focused on one thing. What does appear to be true is that quickly rising interest rates tend to slow home price appreciation.

What Happened When Rates Were the Highest in Recent History?

In 1976, a 30-year fixed-rate mortgage averaged 8.87 percent, with 1.2 points. Rates then hit double digits in 1979 at 11.2 percent with 1.6 points and finally reached an incredible high in 1981 of 16.63 percent, with 2.1 points. That’s an 87.4859 percent increase.

How did prices perform? Surely, they tanked right? Not at all. In January 1976 the median home price was $33,693.12, then by December 1981 the median home price rose to $61,848.27, an incredible 83.565 percent increase.

Right now, rates are above their 2022 average, but historically speaking, mortgage rates appear to be well below their all-time averages. In order to reach their 1981 highs of 16.63 percent, rates would have to skyrocket 155.846 percent higher from current levels.

Now that we’ve put those numbers out there. What about housing prices? Are they in a mega-bubble reaching highs never ever before seen? Are rising rates their demise?

Once again, we need to take a bird’s eye approach as there are so many moving parts that affect prices. Pinning price movement with one factor like interest rates can be considered overly simplistic reasoning.

One must include items like rent prices, inventory levels, employment rates, average income, average debt burdens, foreclosure filings, replacement cost, building costs and so much more.

No one factor can predict the future much less predict it accurately.

The chart below plots both the S&P 500 and the Case-Shiller Home Price Index. Over the long term the S&P 500 clearly outperforms residential property and is more volatile.

According to A Wealth of Common Sense, in general, the stock market enjoys higher than average returns when inflation is falling and below average but when inflation is rising and above average the tables turn.

On the other hand housing does better with higher inflation. When inflation is low housing returns tend to be below average.

While the late 1970s and 80s were rife with inflation, real estate held its own. But what is very clear is that one cannot make sweeping statements or decisions based on one or two factors.

Don’t Stress It. Just Work with Where You Are Today

What matters at the end of the day is that you do what’s right for you and your family. If you are able to buy at current prices, it may not be wise to procrastinate or wait for the sun, moon and starts to align.

We never know what tomorrow brings, but we do know where we are today. But ultimately the decision is yours. If you find yourself in a position to buy or refinance, we’d love to work with you.

Visit one of our local branches or find a loan officer online and review our wide breadth of programs. We’ll work with you every step of the way to find the loan that fits your needs.

Related articles

Real Estate Branding Mistakes Agents Make and How to Build a Stronger Brand

Your brand is often the first thing a potential client notices — and the reason they...

Renting vs. Owning a Home: Why Homeownership Can Be a Smart Long-Term Investment

Choosing between renting and buying is one of the biggest financial decisions...

The Modern Real Estate Toolkit: What Agents Are Using in 2026

Real estate in 2026 moves fast and technology is at the center of it. The agents who...