Refinancing Your Home Equity Loans — Consider Refinancing into a First Mortgage

The current real estate market conditions not only affect buying and selling, but it can even be a challenge for non-sellers. And here’s why.

The non-sellers we’re talking about are homeowners who took advantage of a low interest rate environment and soaring home values to secure a home equity loan.

But fast-forward to today and interest rates on the rise and sales slowing, and there’s a real possibility of a temporary downturn in home values.

With the waters getting choppy, the market conditions may be right to convert your home equity loans into a first mortgage.

Let History Be Your Guide

Home equity loans and lines of credit (HELOC) are primarily tied to your home’s value while a mortgage is typically the lending tool that allows a buyer to purchase (finance) the property.

Generally, a home equity loan is looked at as a second mortgage. This is if the borrower already has an existing mortgage on the home. If the home goes into foreclosure, the lender holding the home equity loan does not get paid until the first mortgage lender is paid. That means the home equity loan lender’s risk is greater, which is why these loans typically carry higher interest rates than traditional mortgages.

On the other hand a borrower who owns their property free and clear may decide to take out a loan against the home’s value. The lender making that home equity loan would be a first lienholder.

Bye-Bye Interest Deductions?

So why would anyone want to convert? Well, you’ll want to hear this!

Under the Tax Cuts and Jobs Act of 2017, interest on a mortgage is tax deductible for mortgages of up to either $1 million (if you took out the loan before Dec. 15, 2017) or $750,000 (if you took it out after that date). This new limit applies to home equity loans as well: $750,000 is now the total threshold for deductions on all residential debt.

Here’s the key to why you may want to convert. Homeowners used to be able to deduct the interest on a home equity loan or a HELOC no matter how they used the money. That’s not the case anymore.

The act suspended the deduction for interest paid on home equity loans from 2018 through 2025 unless they are used to buy, build, or substantially improve the taxpayer’s home that secures the loan.

That’s Why Converting to a Conventional Mortgage May Be A Wise Move

Now no one is screaming doom and gloom. We know over a long period of time home prices rise with inflation. But there are cycles to every market, and you must keep a keen eye on the current conditions.

Many sellers have slashed their asking prices in recent months. In July 2022, Redfin reported, “nearly two-thirds (61.5%) of homes for sale in Boise, ID had a price drop in June, the highest share of the 97 metros in this analysis. Next came Denver (55.1%) and Salt Lake City (51.6%), each metro where more than half of for-sale homes had a price drop.”

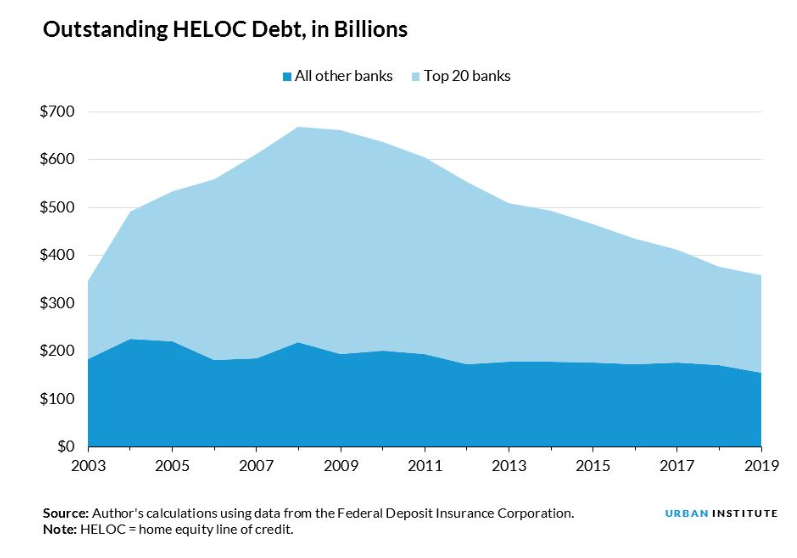

According to Urban Institute, outstanding mortgage debt is $9.4 trillion, the outstanding HELOC debt continues to shrink. In the second quarter of 2019, outstanding HELOC debt was less than $400 billion for the first time since 2004, according to the Federal Reserve Bank of New York. This is down from a peak of $714 billion in 2009. The decline in HELOCs reveals high risk aversion among lenders and consumer cautiousness.

So What Are Your Alternatives?

Rather than refinancing your home equity loan and continuing to have two mortgages, it may be a smart idea to refinance both into a single loan without increasing how much you’re borrowing. You’ll get a new interest rate and a new loan term. It’s more like a loan consolidation.

And in today’s rising interest rate market, the timing may be perfect. You could enjoy:

- A lower interest rate, CNET report, home equity loan rates are hovering around 7% while a 30-year fixed is around 6.1%

- A single monthly payment

- Predictable borrowing costs

- Your home should still appraise well at this time

- Only have a single mortgage lien against your home

- You may be entitled to greater tax benefits (see a qualified advisor)

It’s always important to work with a lender who considers what’s best fits your financial situation. Together you’ll want to focus on:

- The monthly payment and loan term

- The interest rate type (fixed or variable)

- Upfront fees and the total cost

- How stringent the requirements are

All The Lending Solutions and Flexibility You Will Need

Remember, when you decide to work the professionals at Embrace Home Loans behind every loan officer stands a team of dedicated lending professionals, committed to helping you achieve your goals.

Whether it’s converting your home equity loan to a first mortgage or simple refinance, when you need us, we’ll be ready to tailor a loan program just right for you, quickly and professionally.

Contact a local loan officer today to run the numbers and see if this is the right option for you.

Related articles

Tapping the Equity in Your Home for Cash: When a Cash-Out Refinance Might Make Sense

For many homeowners, their home is more than just a place to live. It’s also one of...

How REALTORS® Can Spot Refinance Opportunities and Stay Connected After Closing

Many REALTORS® focus on getting clients to the closing table. The best ones continue...

When Should You Refinance Your Mortgage? Here’s When It May Make Sense

Refinancing isn’t just about chasing a lower interest rate. For many homeowners,...