Does Refinancing Hurt Your Credit?

With the recent rise in interest rates, homeowners who were once eager to refinance might be wondering: is it still worth it? While historically low rates have faded, refinancing may still offer advantages depending on your individual situation and the terms you can secure.

This blog dives into the updated landscape of refinancing, exploring its impact on your credit score and offering crucial tips to navigate the process in a high-interest environment, including steps to keep your credit healthy throughout the journey.

What is refinancing?

At its core, refinancing involves taking out a new loan in order to pay off your old one. Typically, the new loan will have better terms, such as a better interest rate or a different length. Usually, people will refinance as a way to save money. Though, it is also important to note that several types of loans can be refinanced, including student loans, auto loans, and mortgages. Refinancing is often a good alternative to taking out a personal loan or paying off one credit card with another through a balance transfer.

How does refinancing impact your credit?

Refinancing may affect your credit score, but the impact could be less significant in the current environment. Here’s how:

1. Hard inquiries.

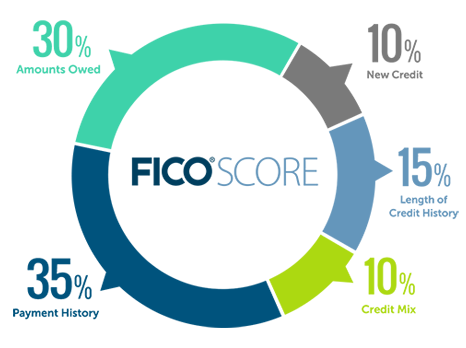

Whenever you ask a mortgage lender to determine whether or not you qualify to refinance, they will pull a copy of your credit report. In particular, hard inquiries will have an impact on your credit score. In fact, the number of inquiries on your credit report count for approximately 10% of your FICO score.

2. Replacing old credit with new credit.

Then, the length of your credit history also impacts your credit score. In this case, we’re talking about how long your mortgage has been open. Unfortunately, when you refinance, you close one of your accounts and replace it with a new one, which ends up shortening the average age of your credit accounts. On the whole, the average age of your credit accounts is 15% of your total score.

3. Late or missed payments.

The last impact that refinancing can have on your credit score can be attributed to human error. Sometimes, when people are in the process of refinancing a loan, they have a tendency to confuse due dates or to be unsure whether they should keep paying their current loan, which can accidentally result in missed payments and have a negative impact on your credit score. For its part, payment history accounts for 30% of your overall score.

How to keep your credit healthy while refinancing

Once you have a better idea of how refinancing can hurt your credit, it’s important to take some time to figure out how to keep your credit healthy during this process. With that in mind, we’ve curated a few tips for you below. Take a look so that you have a better idea of what you can do to ensure that your credit stays in good shape when you refinance your mortgage.

1. Keep making payments until you close on your new loan.

The first and most important thing that you can do if you’re trying to keep your credit in good shape is to keep making payments on your existing loan until the refinance is complete. Typically, refinancing a mortgage will take a little bit of time to complete.

It can generally take up to two months to refinance your mortgage, though it typically takes between 30 to 45 days. But as mentioned earlier, the time it takes will differ per individual.

For instance, the following can affect the refinancing timeline:

- Financial paperwork requirements

- Underwriting process

- Appraisals/inspections

As you may have experienced, the underwriting and appraisal process can take the longest, while other steps — such as providing various financial documents — may not take as long. You can speed up that process by having such documents (e.g., proof of homeowners insurance, paystubs, tax returns, W-2s, and bank statements) readily available.

2. Practice smart rate shopping.

The other thing that you can do is to practice smart rate shopping. Here, it’s important to note that you can try to limit the number of inquiries to show up on your report by applying with all the lenders for every credit check in the same 30-day window. If you make sure to keep track of your time, all of the inquiries for the same item will be counted as one. However, unfortunately, if there is a hard pull on your credit outside of that window, it will count as an additional inquiry.

3. Limit additional applications after refinancing.

In general, it takes two years for an inquiry to fall off your credit report. After refinancing, you’ll want to be sure to limit the number of new credit applications that you put in during that two-year time period after your refinance has been completed. While the impact of the inquiries will lessen over time, having too many inquiries on your credit report at one time can seriously ding your score and make refinancing hurt your credit.

Related articles

Tapping the Equity in Your Home for Cash: When a Cash-Out Refinance Might Make Sense

For many homeowners, their home is more than just a place to live. It’s also one of...

How REALTORS® Can Spot Refinance Opportunities and Stay Connected After Closing

Many REALTORS® focus on getting clients to the closing table. The best ones continue...

When Should You Refinance Your Mortgage? Here’s When It May Make Sense

Refinancing isn’t just about chasing a lower interest rate. For many homeowners,...