High Interest Rates – Are they Here to Stay?

The surge in interest rates has had a significant impact on the real estate market in the USA. Higher borrowing costs have made it more expensive to buy a home, which has dampened demand and led to a slowdown in home sales. The median home price has also started to come down, as buyers have less purchasing power.

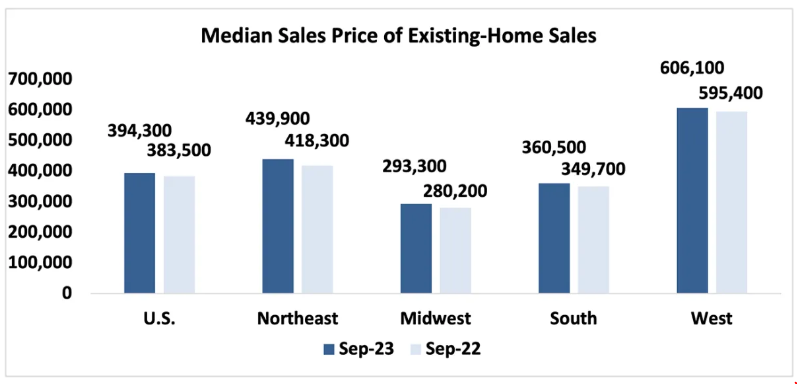

According to the National Association of Realtors (NAR), existing home sales fell by 15.4% in September 2023 compared to September 2022.

The national median existing-home price for all housing types reached $394,300 in September, up 2.8% from a year ago.

This slowdown in the housing market is likely to continue in the near term, as interest rates are expected to remain high. However, some experts believe that prices could start to stabilize or even increase again in the longer term, as demand for housing remains strong.

The Impact of Rising Rates

- First-time homebuyers are having a more difficult time qualifying for mortgages. This is because they typically have lower down payments and therefore need to borrow more money. With higher interest rates, their monthly mortgage payments would be higher, which could make it difficult to afford a home.

- Homeowners who are looking to refinance their mortgages are finding that they may not be able to save as much money as they would have liked. This is because the interest rates on new mortgages are higher than the interest rates on their existing mortgages.

- Investors are becoming more cautious about buying rental properties. This is because higher interest rates make it more expensive to borrow money to purchase a rental property. Additionally, with the slowdown in the housing market, investors may be concerned about the potential for rental vacancies and lower rental income.

The Case for Higher Interest Rates

Proponents of higher interest rates argue that they are necessary to curb inflation and bring it back to central bank targets. Inflation erodes purchasing power and can destabilize economies, so it is crucial to address it promptly and effectively.

Goldman Sachs Research says, “we expect home prices to increase, even as borrowing costs remain elevated. Our new forecast for mortgage rates reflects a steeper yield curve (longer-maturity Treasury yields are rising, which tends to increase mortgage rates) and Treasury yield volatility that remains “stubbornly high.”

According to a September 27, 2023, article by Morgan Stanley, “Markets may have finally gotten the message that the U.S. Federal Reserve is planning to keep rates higher for longer. While inflation has thus far come down faster than expected core inflation around 4% is still far from the Fed’s target, and a strong labor market makes further inflation progress uncertain.”

The Case for Lower Interest Rates

Ralph DiBugnara, president at Home Qualified, “It looks like we have had the first major shift downwards for rates in a while. In October, U.S. payrolls came in lower than anticipated, which is a good sign that inflation may have reached its peak and could trigger a lowering of rates. I expect the Fed to stay neutral for the remainder of the year with any rate cuts coming in the first quarter of 2024. For December I believe the average 30-year fixed rate will land at 7.65% and the 15-year fixed will be 6.99%.”

Danielle Hale, chief economist at Realtor.com, “Mortgage rates are positioned to decline in November, and the streak may continue into December if the next few inflation readings come in as expected. Already, longer-term rates on bonds like the 10-year treasury have begun to decline in anticipation of the possibility that the Fed has done enough to cool the economy and tame inflation. Mortgage rates are likely to follow suit.”

Wells Fargo, “In its latest U.S. Economic Outlook, Wells Fargo puts the 30-year conventional mortgage rate at 7.3% in the fourth quarter of 2023, declining somewhat to 7% at the beginning of next year. The bank’s forecasting group predicts that rates will fall below 6% at the end of 2024.”

The question of whether high interest rates are here to stay remains unanswered. Central banks will continue to monitor economic data closely and adjust their policies accordingly. The future of interest rates will depend on the effectiveness of their efforts to combat inflation and steer the economy towards a sustainable growth path.

Personalized Guidance to Meet Your Needs Regardless of Market Conditions

In these uncertain times of fluctuating interest rates and economic dynamics, it’s crucial for buyers, those looking to refinance, or those wanting to tap into their home equity to have a trusted partner by their side. Embrace Home Loans® offers a wealth of experience and expertise in navigating the ever-changing mortgage landscape.

With personalized guidance and a commitment to helping clients make informed decisions, Embrace Home Loans can provide the support and solutions needed to make the most of the current real estate market conditions.

Don’t hesitate to reach out to Embrace Home Loans and secure your financial future today.

Related articles

Mortgage Rates Move Up and Applications Fall

On Wednesday, July 29, 2026, Optimal Blue released its rate indices showing the 30-year...

How Airbnb and Short-Term Rentals Are Affecting Local Housing Markets

Short-term rentals have become a major part of today’s housing market. Platforms...

2026 Spring Housing Market Forecast — What Buyers & Sellers Should Know

The 2026 U.S. housing market is expected to look quite different from recent years of...